By Brian Gass, Executive Director, Real Housing Reform Initiative

On March 30, 2026, Governor Bob Ferguson signed Senate Bill 6346 into law, creating Washington State's first broad-based income tax since the 1930s.

Despite a century of constitutional prohibition, despite voters rejecting income taxes ten times over ninety years, despite Washington's identity as one of just nine states without an income tax—the millionaire tax is now law.

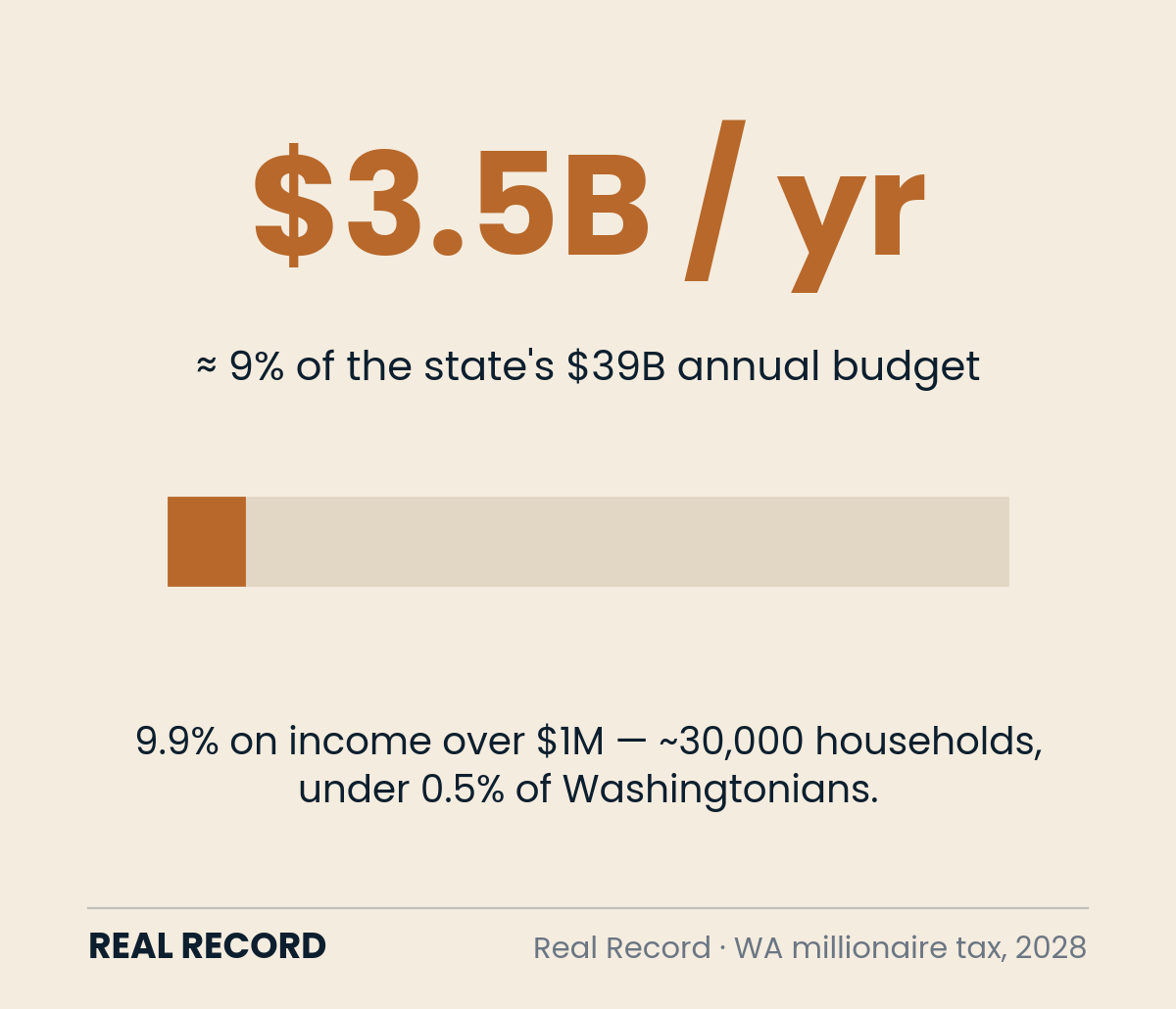

Effective January 1, 2028, Washington will impose a 9.9% tax on income over $1 million per household. Proponents estimate it will raise $3.5 billion annually, affecting approximately 30,000 households—less than 0.5% of Washington residents.

But make no mistake: this isn't just about taxing millionaires. It's the first crack in a constitutional wall that has stood for nearly a century. And once that wall falls, it never goes back up.

What the Millionaire Tax Actually Does

The official name is the "Washington Millionaires' Tax," codified in Senate Bill 6346. Here's how it works:

The Basic Structure

Rate: 9.9% on Washington taxable income over $1 million

Threshold: $1 million per household (same for single and joint filers)

Effective: January 1, 2028

First payments due: April 2029

"Washington taxable income" is defined as federal adjusted gross income (AGI) with certain adjustments.

Example Calculation

You're a household with $1.5 million in AGI:

- First $1 million: not taxed (standard exemption)

- Next $500K: 9.9% tax = $49,500

A household with $3 million in AGI:

- First $1 million: not taxed

- Next $2 million: 9.9% tax = $198,000

What Income Is Included

The tax applies to all income types:

- Wages and salaries over $1M

- Business income (including pass-through from LLCs, S-corps, partnerships)

- Investment income (interest, dividends, capital gains)

- Rental income

- Royalties and licensing fees

- Retirement distributions (from IRAs, 401(k)s, pensions)

This is a true income tax, not an excise tax on specific transactions like the capital gains tax. It applies to all income over the threshold, regardless of source.

Who's Subject to the Tax

The tax applies to:

- Washington residents: All income, regardless of where earned

- Part-year residents: Income earned while living in Washington

- Nonresidents: Income sourced to Washington (business operations, rental property, etc.)

If you work remotely for a Washington company but live in Oregon, your income isn't subject to the tax. But if you're a Washington resident earning income from an Oregon employer, it is.

Exemptions and Deductions

Unlike the capital gains tax (which exempts real estate), the millionaire income tax has fewer exemptions:

Standard deduction: $1 million per household

Charitable deduction: Allowed under certain circumstances

Retirement account deduction: Potentially available (details TBD)

Notably, the millionaire tax does NOT exempt:

- Real estate income (rental income is fully taxable)

- Real estate capital gains (taxable as income)

- Business income from any industry

This is broader than the capital gains tax, though the $1M threshold means most people will never pay it.

The Revenue Promise: $3.5 Billion Annually

Proponents estimate the tax will generate $3.5 billion per year starting in 2029. To put that in context:

- Washington's current biennial budget: ~$78 billion

- Annual budget: ~$39 billion

- Millionaire tax: ~9% of annual state budget

That's not trivial revenue. It's enough to:

- Fund the entire Department of Social and Health Services

- Double the state's higher education budget

- Pay for K-12 education increases for years

But here's the critical question: where does that $3.5 billion actually go?

The Spending Plan: Tax Cuts and Investments

The millionaire tax legislation allocates revenue across several categories:

Phase 1 (2029): 41.3% returned to taxpayers via tax cuts

Phase 2 (2030+): 47.3% returned to taxpayers

Specific allocations include:

- Working Families Tax Credit expansion: Increased EITC-style credit reaching 460,000+ additional households

- Small business tax relief: B&O tax reductions for businesses under certain thresholds

- Sales tax exemptions: Diapers, feminine hygiene products, certain groceries

- K-12 education: Free breakfast and lunch for all students

- Childcare subsidies: Expanded access to early learning programs

- General fund: The remaining 52.7%+ for education, healthcare, and other services

The legislation is structured to demonstrate that millionaire tax revenue goes back to working families, not just general government growth.

The Constitutional Hurdle: How They Did It

Washington's constitution has long been interpreted to prohibit income taxes. Article VII, Section 1 requires that "all taxes shall be uniform upon the same class of property."

The Washington Supreme Court has consistently ruled that this means:

- Property must be taxed uniformly (no graduated rates)

- Income is property

- Therefore, graduated income taxes are unconstitutional

This interpretation has held since the 1930s. It's why Washington has no income tax despite repeated efforts.

So how did SB 6346 get around this?

The Legal Strategy: Three Prongs

Prong 1: The Capital Gains Precedent

The 2023 Washington Supreme Court decision in Quinn v. State of Washington upheld the capital gains tax by ruling it was an excise tax on transactions, not an income tax.

The millionaire tax uses similar language: it's technically an excise tax on the privilege of earning high income in Washington, not a direct tax on income itself.

This is semantic gymnastics, but it mirrors the capital gains tax framework the court already blessed.

Prong 2: The Threshold Defense

By setting the threshold at $1 million, the tax applies uniformly to all income over that amount. The argument: everyone above $1M pays the same rate (9.9%), so it's uniform within that class.

This distinguishes it from a fully graduated income tax with multiple brackets. It's one rate, one threshold—technically "uniform."

Prong 3: The Deference Doctrine

Courts generally defer to the legislature on tax policy. Unless a tax is clearly unconstitutional, judges are reluctant to overturn it.

The capital gains tax survived judicial review. The millionaire tax's sponsors bet that courts will extend the same deference here.

Will It Survive Legal Challenge?

Absolutely it will be challenged. Within weeks of the governor's signature, lawsuits were filed arguing:

- The tax violates uniformity requirements

- The "excise tax" framing is a transparent fiction

- The capital gains precedent doesn't extend to broad-based income taxes

But the reality is this: the composition of the Washington Supreme Court has shifted. Justices who might have struck down an income tax in the 1990s have been replaced by justices more sympathetic to progressive taxation.

Prediction: The tax survives judicial review, 5-4 or 6-3.

The Initiative Threat: Can Voters Repeal It?

Even if the tax survives judicial review, voters could potentially repeal it via initiative.

But there's a catch: the Washington State Constitution (Article II, Section 1) states that measures "necessary for the immediate support of the state government and its existing public institutions" cannot be subject to referendum.

The millionaire tax legislation includes language declaring the tax essential to funding education, healthcare, and core government services. Legislative Democrats argue this makes it referendum-proof.

Opponents disagree, claiming this is an abuse of the "essential government function" exception. They're pursuing a ballot initiative anyway, arguing that a new tax isn't "existing" support.

Status as of May 2026: Initiative campaigns are gathering signatures. If they collect enough by July 2026, the question goes to voters in November 2026.

But here's the twist: even if an initiative qualifies, it can't take effect until after the tax itself takes effect in 2028. Washington would have at least two years of millionaire tax revenue before voters could repeal it.

Once revenue flows in, once budgets are built around it, once services are funded by it—politically, it becomes much harder to repeal.

The "$1 Million Floor" Promise: Can It Hold?

Governor Ferguson and legislative sponsors have repeatedly pledged: "This tax will never apply to income under $1 million."

Some legislators proposed a constitutional amendment to enshrine the $1M threshold, preventing future legislatures from lowering it.

That amendment didn't pass.

Instead, we have verbal promises. And those promises are worth exactly nothing.

Here's what history tells us:

Case Study: The Federal Income Tax

When the 16th Amendment enabled federal income tax in 1913, it applied only to the wealthiest Americans—less than 1% of households.

Original rates: 1% on income over $3,000 (~$95,000 in 2026 dollars), rising to 7% on income over $500,000.

Within a decade, rates hit 77%. By World War II, they reached 94%. The threshold dropped so low that most working families paid income tax.

Today, federal income tax applies to roughly 90% of households, with rates from 10% to 37%.

The promise: "Just the rich will pay."

The reality: Fifty years later, almost everyone pays.

Case Study: California's "Millionaire Tax"

In 2004, California passed Proposition 63, creating a 1% surcharge on income over $1 million to fund mental health services.

The pledge: "Permanently limited to millionaires."

What happened:

- 2012: Threshold lowered to $250K for certain purposes

- 2016: Rates increased to 1.5%

- 2021: Rates increased to 2%

- Multiple attempts to expand the base continue

The original $1M threshold held for the mental health surcharge specifically, but California added numerous other high-earner taxes with lower thresholds.

The Washington Pattern

Washington has a habit of "temporary" or "limited" taxes that expand:

Sales tax: Started at 2% in 1935 (temporarily, to fund schools). Now 6.5% state rate plus local add-ons up to 4%.

B&O tax: Started with simple rates. Now has dozens of classifications, surcharges, and tiers.

Capital gains tax: Started at 7% on gains over $250K (2022). Added 9.9% tier on gains over $1M (2025). More tiers coming.

The pattern is clear:

- Introduce tax with high threshold or low rate

- Build budget dependence on the revenue

- Face shortfall a few years later

- Lower threshold or raise rates to cover gap

- Repeat

The millionaire tax will follow the same trajectory. Five years, maybe ten—the $1M threshold will fall.

The Pass-Through Problem: Double Taxation Squared

One underappreciated impact: how the millionaire tax interacts with Washington's B&O tax and the federal tax system.

Consider a business owner with pass-through income from an S-corporation:

Step 1: Business pays B&O tax on gross revenue (0.471% - 7.5% depending on classification)

Step 2: Remaining profit flows to owner as taxable income

Step 3: Owner pays Washington millionaire tax (9.9% on income over $1M)

Step 4: Owner pays federal income tax (up to 37%)

Step 5: Owner pays Medicare tax (3.8% surtax on investment income)

A small business owner in advanced computing could face:

- 7.5% B&O tax on company gross revenue

- 9.9% Washington millionaire tax on net income over $1M

- 37% federal income tax

- 3.8% Medicare surtax

That's 58.2% combined marginal tax rate, not counting local B&O taxes and property taxes.

At what point does it make more sense to move the business to Texas or Florida?

The Migration Question: Will High Earners Leave?

Opponents argue the millionaire tax will drive high earners out of state. Supporters say evidence from other states shows minimal migration.

Both are partially right.

What Research Shows

Studies on high-earner migration to avoid state income taxes find:

- Young, mobile workers: More likely to relocate (especially tech workers, traders, freelancers)

- Established families: Less likely to relocate (schools, community ties, home equity)

- Retirees: Moderately likely to relocate (no job ties, fixed income)

The effect is real but not dramatic. California, New York, and Massachusetts maintain high-earner populations despite high tax rates.

But the effect compounds over time. Washington doesn't lose every millionaire overnight. It loses:

- The marginal entrepreneur who was considering where to start their company

- The executive who was deciding between Seattle and Austin

- The retiree who was on the fence about Bellevue vs. Scottsdale

Over a decade, that adds up.

The Amazon/Microsoft Lock-In

Washington has one massive advantage: Amazon and Microsoft headquarters.

These companies employ tens of thousands of high earners who can't easily relocate. Even with remote work, senior executives need to be near headquarters. Engineers want to work in-office for collaboration and visibility.

This creates a captive high-earning population that will pay the millionaire tax regardless of whether they like it.

But it also means Washington's tax policy is dependent on two companies remaining committed to the state. If Amazon or Microsoft ever significantly relocates operations, the millionaire tax revenue collapses.

The Real Endgame: Universal Income Tax

Here's the part supporters won't say out loud: the millionaire tax is a stepping stone to a universal income tax.

The legislative sponsors know it. The governor knows it. Everyone paying attention knows it.

Here's how it plays out:

2028-2029: Tax takes effect, generates $3.5B annually

2030: Budget incorporates that revenue as baseline

2032: Economic downturn or spending increase creates $4B shortfall

2033: Legislators face choice: cut services or expand millionaire tax

2034: Threshold lowered to $500K ("just high earners")

2036: Threshold lowered to $250K ("still just upper middle class")

2038: Threshold lowered to $100K ("almost everyone else has an income tax, why not us?")

By 2040, Washington has a full income tax with brackets from $50K to $5M+, rates from 3% to 12%, and the original $1M threshold is a distant memory.

The millionaire tax breaks the political and legal barriers to income taxation. Once those barriers fall, there's no mechanism to prevent expansion.

Why Wayfair, B&O, Capital Gains, and Millionaire Tax Are All Connected

This blog post is part of a series examining Washington's tax structure. To understand why these pieces fit together, consider the pattern:

Wayfair (2018)

Problem: E-commerce eroding sales tax base

Solution: Economic nexus captures online sales tax

Result: Sales tax base protected, billions in new revenue

B&O Tech Surcharges (2025)

Problem: Budget shortfall, need immediate revenue

Solution: 7.5% surcharge on advanced computing (Amazon, Microsoft)

Result: $400M+ annually from companies that can't easily leave

Capital Gains Tax (2022)

Problem: Need progressive revenue source

Solution: 7% (now 9.9%) tax on stock sales, exempt real estate

Result: $500M+ annually, property tax base protected

Millionaire Income Tax (2028)

Problem: Next budget shortfall, political pressure for tax fairness

Solution: 9.9% tax on income over $1M

Result: $3.5B annually, path to universal income tax

The pattern: Washington identifies revenue sources, taxes them aggressively, protects core revenue streams (sales, property), and expands over time.

Real estate remains exempt from capital gains tax because property tax generates $18B annually. Sales tax expansions (services) capture the shift from goods to digital economy. B&O surcharges extract maximum revenue from captive industries. And now, the millionaire income tax opens the door to taxing all income.

It's not random. It's a deliberate, systematic approach to revenue maximization while protecting the base.

Conclusion: The Tax That Changes Everything

The millionaire income tax is Washington's most significant tax policy change in 90 years.

It's not significant because it raises $3.5 billion—Washington has added larger revenue packages before.

It's significant because it fundamentally alters what's politically and legally possible in Washington tax policy.

Before March 30, 2026, Washington couldn't have an income tax. The constitution prohibited it, the courts enforced it, and voters rejected it repeatedly.

After March 30, 2026, Washington has an income tax. It's narrow for now—just high earners—but the infrastructure, precedent, and political will are established.

The threshold will fall. The rates will rise. Within fifteen years, Washington will have a full income tax system rivaling California and New York.

And when that happens, remember: it started with a promise that only millionaires would pay.

Read the full series:

- The Wayfair Windfall: How a Supreme Court decision quietly reshaped Washington's tax system

- The Tech Tax: Washington's B&O surcharges target big tech

- The Capital Gains Tax That Doesn't Touch Capital: Why real estate gets a pass

- The Millionaire Income Tax (this post)

Sources:

- SB 6346 (2026) - Washington State Legislature

- Governor Ferguson signing statement and materials

- Washington State Economic and Revenue Forecast Council projections

- Quinn v. State of Washington (2023) - Washington Supreme Court

- Various analyses from Clark Nuber, BDO, Washington Senate Democrats, ITEP

Real Housing Reform Initiative

Government meetings belong to the people. So does the information inside them.

Comments