By Brian Gass, Executive Director, Real Housing Reform Initiative

When most Washington residents think about state taxes, they think about the ongoing debates over income taxes, capital gains taxes, or millionaire taxes. But in 2018, a seemingly technical Supreme Court case about online sales tax fundamentally transformed how Washington collects revenue—and most people never noticed.

The decision in South Dakota v. Wayfair didn't just level the playing field between brick-and-mortar stores and online retailers. It opened a multi-billion-dollar revenue stream that now props up Washington's entire tax structure. Understanding Wayfair is essential to understanding why Washington's tax system is structured the way it is today.

What Wayfair Changed

For decades, the rule was simple: states could only require businesses to collect sales tax if they had a physical presence—a store, warehouse, or office—in that state. This "physical presence rule" came from a 1992 Supreme Court case called Quill Corp. v. North Dakota.

As e-commerce exploded, states watched billions in potential sales tax revenue slip through their fingers. Amazon, Wayfair, Overstock, and thousands of other online retailers sold products to state residents without collecting a dime in sales tax. Technically, consumers owed "use tax" on these purchases, but individual compliance was virtually non-existent.

On June 21, 2018, the Supreme Court overturned the physical presence rule in South Dakota v. Wayfair, Inc. The decision introduced the concept of "economic nexus"—the idea that a business's economic activity in a state creates a tax obligation, even without any physical presence.

South Dakota's law, which the Court upheld, was straightforward: if a business had more than $100,000 in sales OR 200 or more transactions in the state, they had to collect sales tax. The Court found these economic connections sufficient to establish "substantial nexus" under the Commerce Clause.

Washington's Swift Response

Washington State didn't wait. The Department of Revenue moved with remarkable speed.

October 1, 2018: Washington implemented its economic nexus standard, matching South Dakota's thresholds. Remote sellers with more than $100,000 in sales OR 200 transactions had to register and collect sales tax.

March 14, 2019: The Legislature simplified things by removing the transaction count. The threshold became a clean $100,000 in annual gross retail sales.

January 1, 2020: The state extended economic nexus to the Business and Occupation (B&O) tax, using the same $100,000 threshold based on cumulative gross receipts.

But Washington actually had a head start. Since January 2018—before the Wayfair decision—the state had required remote sellers with just $10,000 in sales to either collect sales tax OR comply with use tax notice and reporting requirements. Wayfair simply gave Washington the constitutional green light to enforce full collection requirements on larger sellers.

The Revenue Impact: Billions in New Collections

The numbers are staggering.

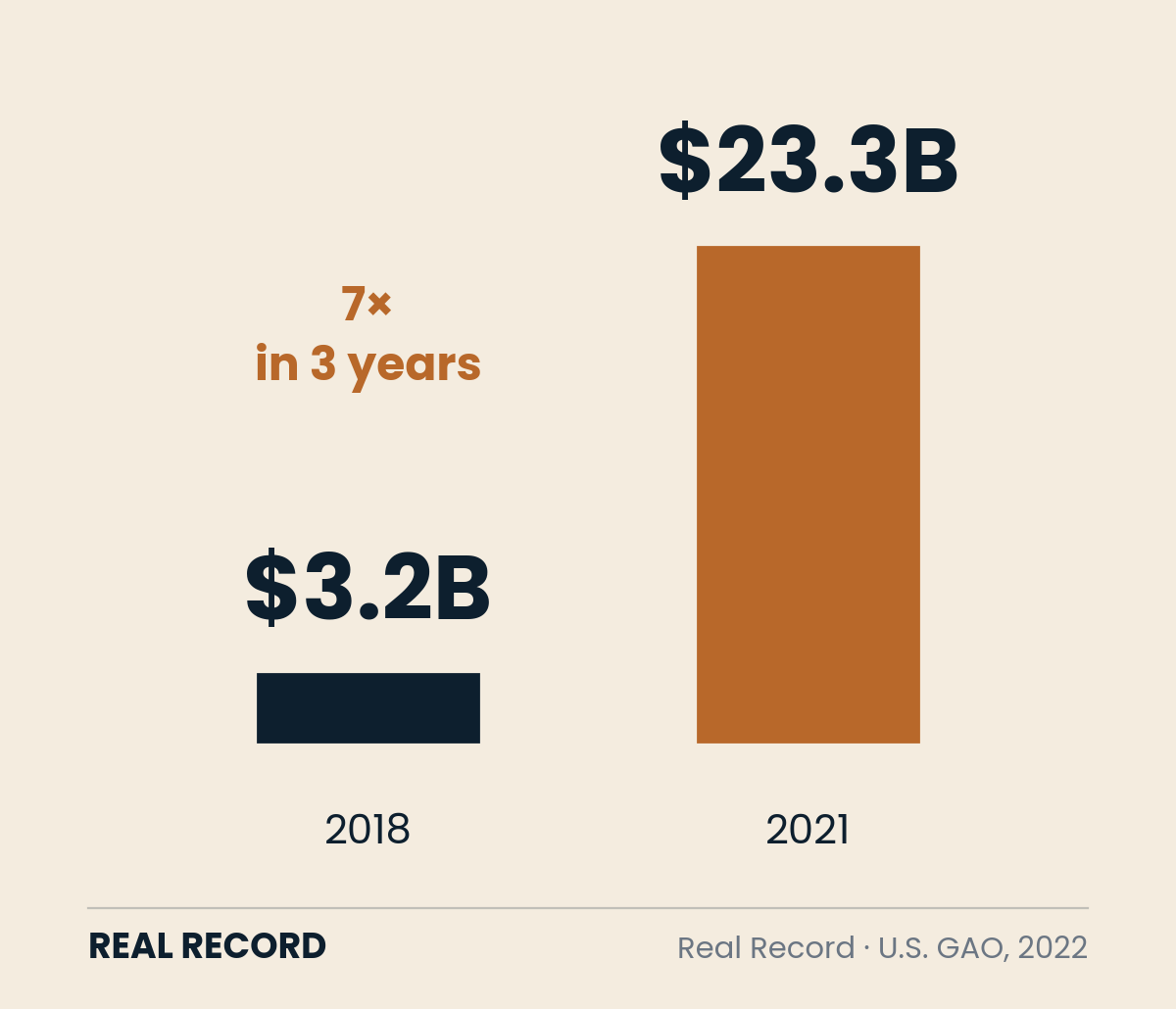

According to a U.S. Government Accountability Office survey, states collected $23.3 billion from remote sellers in 2021, up from just $3.2 billion in 2018—a more than sevenfold increase in three years.

Academic research found that Wayfair increased state sales tax revenues by an average of 7.9 percent. For Washington State, with its heavy reliance on sales tax, this represented hundreds of millions in additional annual revenue.

Consider the timing. Washington's taxable retail sales reached:

- $178.5 billion in 2020 (slight COVID decline)

- $210.4 billion in 2021 (17.9% increase over 2020)

The post-Wayfair surge coincided perfectly with the pandemic's shift to online shopping. While states faced budget crises from business closures, Wayfair ensured sales tax revenues kept flowing from the e-commerce boom.

Why This Matters for Washington

To understand Wayfair's significance, you need to understand Washington's unique tax structure.

Washington is one of just seven states with no personal income tax. The state also has no corporate income tax. Instead, Washington relies more heavily on excise taxes—particularly sales tax—than almost any other state.

According to the Office of Financial Management, Washington ranked 2nd in the nation in per capita state and local sales tax collections in 2023, just behind Hawaii. Sales taxes fund roughly half of the state's operating budget, which pays for schools, parks, prisons, mental health services, and other programs.

This makes Washington's tax base uniquely vulnerable to two threats:

- Economic downturns that reduce consumer spending

- E-commerce shifts that move purchases away from tax-collecting retailers

Wayfair eliminated the second threat. By capturing online sales tax, Washington secured its largest revenue stream against the structural shift to e-commerce.

Beyond Sales Tax: The B&O Tax Expansion

Wayfair's influence extended beyond sales tax. The decision gave states confidence to assert economic nexus for income taxes, franchise taxes, and gross receipts taxes.

Washington seized this opportunity with its Business and Occupation (B&O) tax—a unique gross receipts tax that applies to business activities within the state. Starting January 1, 2020, remote businesses with more than $100,000 in Washington-sourced gross receipts became subject to B&O tax, even with no physical presence in the state.

This was a significant expansion. Unlike sales tax (collected from consumers), B&O tax is paid directly by businesses on their gross revenue. For companies with thin profit margins, the impact can be substantial—and it applies whether the business is profitable or not.

The Political Economy of Tax System Design

Here's where Wayfair connects to the bigger picture of Washington's tax system.

When legislators debate whether to implement a capital gains tax or a millionaire tax, they often frame it as "tax fairness" or "progressive taxation." But there's another dynamic at play: protecting the sales tax base.

Think about it: Washington's tax system is built on a foundation of sales and property taxes. Sales tax brings in roughly half the state budget. Property tax generates approximately $18 billion annually across state and local governments.

Any tax that could potentially threaten these core revenue streams—whether through reduced economic activity or political backlash—faces an uphill battle. Conversely, any revenue source that protects or enhances these streams gets locked in quickly.

Wayfair did exactly that. By ensuring remote sellers collect sales tax, the decision:

- Protected sales tax revenue from e-commerce erosion

- Eliminated the competitive disadvantage for in-state retailers

- Expanded the B&O tax base to out-of-state businesses

- Required no new legislation or voter approval

This wasn't a tax increase in the traditional sense—it was enforcement of existing taxes on transactions that had been going untaxed. No one had to vote on it. No initiative campaign could challenge it. The Supreme Court simply removed a constitutional barrier, and Washington's Department of Revenue implemented the new rules within months.

The Real Estate Exemption Context

This efficient capture of online sales tax revenue stands in stark contrast to how Washington treats real estate gains.

While the state moved with lightning speed to capture sales tax on e-commerce transactions—some of which are quite small—it has maintained broad exemptions for real estate transactions under both the capital gains tax and various proposed wealth taxes.

The 2021 capital gains tax, which taxes gains exceeding $250,000 at 7%, explicitly exempts real estate. When voters passed Initiative 2109 to repeal the capital gains tax in 2024 (which ultimately failed), the debate centered on whether it was an "income tax" or an "excise tax"—but no one seriously proposed removing the real estate exemption.

Why? Because real estate transactions generate massive property tax revenue through:

- Property tax on the underlying assets (ongoing annual revenue)

- Real estate excise tax (REET) on sales transactions

- Economic activity that supports sales tax revenue

Taxing real estate capital gains could theoretically reduce transaction velocity, which might impact these revenue streams. Meanwhile, taxing remote seller transactions posed no such risk—in fact, it eliminated a market distortion that had been hurting in-state retailers.

Marketplace Facilitators: The Amazon Provision

One often-overlooked aspect of Wayfair is how it shifted tax collection obligations to marketplace facilitators.

Most states, including Washington, now require platforms like Amazon, eBay, and Etsy to collect and remit sales tax on behalf of their third-party sellers. This is enormously efficient from a tax collection standpoint—instead of tracking down thousands of individual sellers, the state deals with a handful of large platforms.

The GAO survey found that of the $23.3 billion collected from remote sellers in 2021, approximately $9.8 billion came specifically from marketplace facilitators. This represents 21 states reporting; only five states reported such data in 2018, amounting to just $344 million.

For Washington consumers, this means virtually all online purchases now include sales tax, whether from Amazon directly, a third-party Amazon seller, or an independent online retailer. The "sales tax advantage" that once made online shopping cheaper has effectively disappeared.

The Compliance Burden: Who Pays?

While states gained billions in new revenue, businesses faced substantial new compliance costs.

Every state with a sales tax now has economic nexus laws, but no two states' laws are identical. Different thresholds, different tax rates, different filing requirements, different definitions of taxable goods and services.

For large companies with sophisticated tax departments, this is manageable. For small businesses selling online, it's a nightmare. A small business in Bellingham selling handmade products on Etsy could suddenly owe sales tax in 45 different states, each with its own rules, rates, and deadlines.

Congress has held hearings on the compliance burden, with small business owners testifying about the complexity and cost. The Streamlined Sales and Use Tax Agreement—a pre-Wayfair initiative to simplify multi-state tax compliance—has gained only one new member since 2018. Large states like California and New York remain outside it.

The result? Another advantage for large corporations over small businesses. Amazon handles multi-state tax compliance as a routine part of operations. A sole proprietor selling online struggles with compliance software costs and the constant fear of audits.

Five Years Later: What Wayfair Accomplished

As we approach the sixth anniversary of Wayfair, the decision's impact is clear:

For States:

- Billions in new annual revenue without raising tax rates

- Sales tax base protected against e-commerce erosion

- Stronger budget positions during economic volatility

- Legal foundation for economic nexus across multiple tax types

For Consumers:

- Near-universal sales tax collection on online purchases

- Level playing field between online and in-store prices

- No significant change in total tax burden (the tax was always owed)

For Businesses:

- Substantial new compliance obligations for remote sellers

- Competitive disadvantage for small businesses vs. large platforms

- Economic nexus for multiple tax types (sales, B&O, franchise)

- Increased state audit activity and enforcement

For Washington State Specifically:

- Massive protection of its primary revenue source

- B&O tax expansion to out-of-state businesses

- Stronger negotiating position with large online retailers

- Foundation for future service taxation expansion

The Larger Tax Policy Question

Wayfair raises a fundamental question about tax system design: When states face revenue shortfalls, where do they look first?

The answer reveals priorities:

- Wayfair implementation: Completed in months, no legislation needed

- Sales tax expansion to services: Ongoing, with major expansions in 2025

- B&O tax increases: Regular component of budget negotiations

- Capital gains tax: Years of debate, legal challenges, still includes real estate exemption

- Wealth taxes: Proposed repeatedly, never implemented

- Income tax: Constitutionally prohibited

The pattern is clear: Washington aggressively pursues revenue sources that protect or expand its core sales tax and property tax base. Revenue sources that might threaten these bases—or face organized political opposition—face much higher barriers.

Wayfair didn't just give states the authority to tax remote sales. It demonstrated how quickly and decisively government can act when the revenue stakes are high enough and the political opposition is diffuse.

Looking Forward: The Service Tax Frontier

The next frontier is already here. In the 2025 legislative session, Washington passed the largest tax increase in state history—a $9.4 billion revenue package that expanded sales tax to numerous business services previously exempt.

Effective October 1, 2025, Washington sales tax now applies to many professional and business services. This mirrors Wayfair's logic: as the economy shifts from goods to services, the sales tax base must expand to maintain revenue.

The economic nexus rules established by Wayfair apply equally to these newly taxable services. An out-of-state consulting firm with over $100,000 in sales to Washington clients must now collect sales tax on those services—even with no physical presence in Washington.

Conclusion: The Tax System No One Sees

Most Washingtonians have no idea how much their tax system changed in 2018. There were no ballot measures, no initiative campaigns, no dramatic legislative floor debates. Just a Supreme Court decision, followed by swift administrative implementation.

Yet Wayfair fundamentally reshaped Washington's fiscal landscape. It secured hundreds of millions in annual revenue, protected the state's primary tax base against e-commerce erosion, and established legal foundations for future tax expansions.

When you hear debates about capital gains taxes, wealth taxes, or income taxes, remember: the largest revenue expansion in recent Washington history happened quietly, through a Supreme Court case about online furniture sales.

The question isn't whether Washington will protect its sales tax base—Wayfair proved the state will act decisively when that revenue is at stake. The question is what other revenue sources exist primarily to protect that base, and what exemptions persist to ensure core revenue streams remain unthreatened.

Real estate's exemption from the capital gains tax isn't an accident. It's a feature of a tax system designed to protect property tax revenue above all else. Wayfair just proved how fast Washington can move when the alternative is losing billions in tax collections.

This is part of an ongoing investigation into Washington State's tax system structure. Future articles will examine the relationship between property tax revenue, real estate exemptions, and subsidy programs in Whatcom County and beyond.

Sources:

- South Dakota v. Wayfair, Inc., Dkt. No. 17-494 (U.S. Supreme Court, June 21, 2018)

- Washington Department of Revenue, "Wayfair's Impact on the Marketplace Fairness Act"

- U.S. Government Accountability Office, "State Revenue from Remote Sellers" (2022)

- Washington Office of Financial Management, "Revenue Trends" (2025)

- Washington Department of Revenue, "Tax Statistics" (2018-2021)

- Various academic and industry analyses cited in text

Real Housing Reform Initiative

Government meetings belong to the people. So does the information inside them.

Comments