An investigation into how Washington's landmark education funding case became the state's largest property tax increase—and why schools still say they're broke

The Constitutional Promise

Article IX, Section 1 of the Washington State Constitution declares it "the paramount duty of the state to make ample provision for the education of all children residing within its borders." Simple words. Clear obligation.

In 2007, two families filed a lawsuit claiming Washington wasn't meeting that duty. By 2012, the state Supreme Court agreed. Judge John Erlick's ruling was blunt: "State funding is not ample, it is not stable, and it is not dependable."

The court's solution? Force the legislature to fully fund basic education through "regular and dependable tax sources"—meaning state dollars, not local levies. The justices held the legislature in contempt and imposed a $100,000-per-day fine that lasted over five years.

In 2018, after billions in new state funding, the court declared victory and closed the case.

But here's what they don't tell you: The McCleary "solution" was the largest property tax shift in modern Washington history—and it set up a funding structure that would drive your property taxes higher while leaving school districts claiming they're still underfunded.

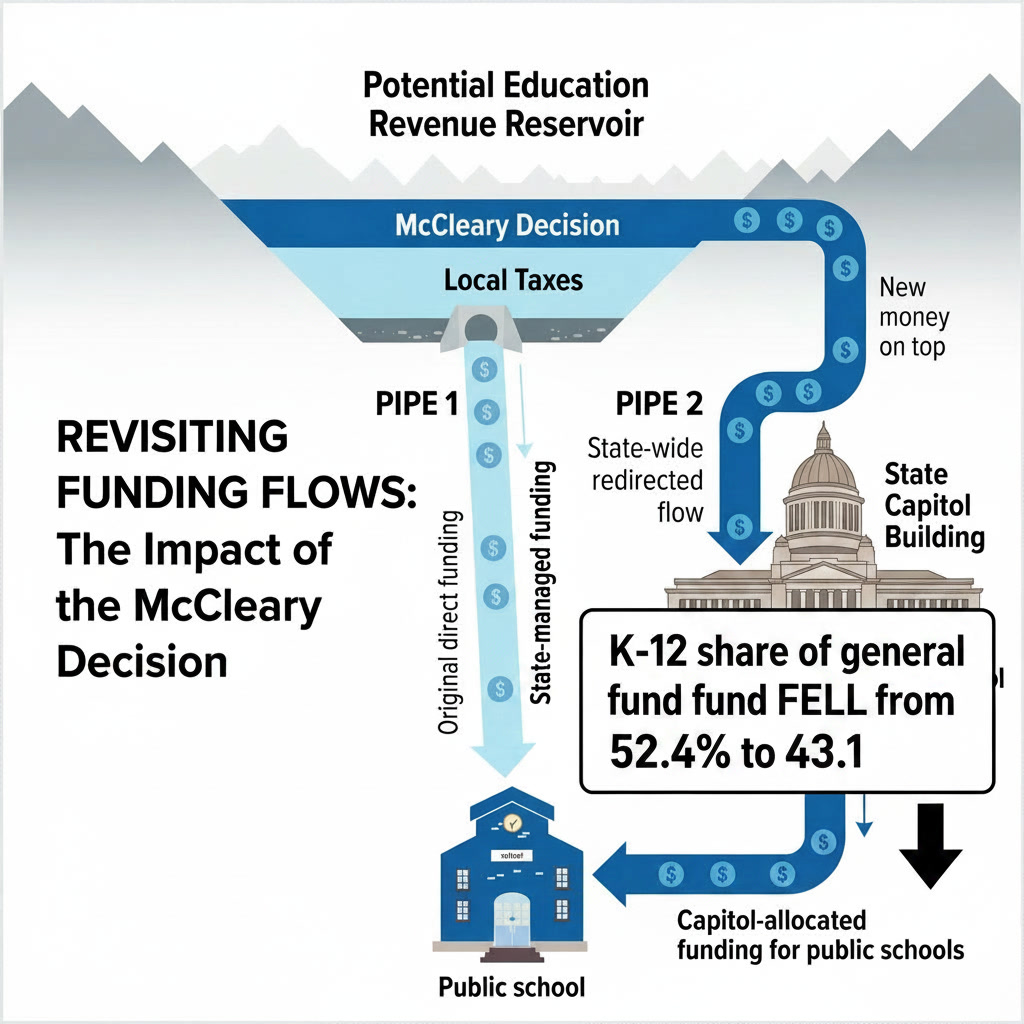

Following The Money: What Actually Happened

Let's start with the numbers everyone cites: Per-student spending jumped from roughly $10,000 in 2012-13 to over $19,000 by 2024—an 80% increase in just over a decade.

Washington now ranks in the top 20 states for education spending per student. Average teacher salaries rose to become the fifth highest in the country.

Mission accomplished, right?

Not quite. Because while the state increased funding, it also fundamentally restructured how schools are financed—and the result was a property tax shuffle that increased total collections while creating new funding gaps.

The Property Tax Shell Game

Here's how the shell game works:

Before McCleary: School districts relied heavily on local levies. Property-rich districts like Seattle could generate more per student than property-poor districts like Federal Way. The court called this unconstitutional.

The "Fix": The legislature increased state education funding through higher state property taxes while capping local levies. Local enrichment levies were capped at $2.50 per $1,000 of assessed property value, with a maximum of $2,500 per student (adjusted for inflation, now around $2,606).

But here's the trick: The state property tax increase was larger than the local levy reduction. Your total education property tax burden went up—it just got relabeled as "state" funding instead of "local" funding.

The Legislature passed a new state tax to pay for basic education while simultaneously capping local levies. From a taxpayer perspective, you're still writing the same check—the payee just changed from "Local School District" to "State of Washington."

The Levy Cap Paradox

The levy cap created an immediate crisis. Districts hitting the revenue cap of $2,606 per student lose local revenues with declining enrollment, while rate-capped districts (those in less wealthy areas) don't lose revenues when enrollment drops because they never hit the cap in the first place.

The inequity the court wanted to fix? It's still there—just inverted. Research shows wealthier school districts saw greater funding increases following McCleary, but now also face bigger budget pressures from declining enrollment.

The legislature's response? They lifted the levy caps in 2019, allowing districts to ask voters for more local property tax increases—exactly what McCleary was supposed to prevent.

So we're back to local levies funding schools. Except now the state property tax is also higher. Both went up.

The Outcomes Question

Here's where the story gets uncomfortable for proponents of the "more money solves everything" approach.

Total per-student spending increased 148% from 2012-13 to 2022-23—a growth rate that "exceeds both the Seattle Consumer Price Index (CPI) and Implicit Price Deflator (IPD)."

Yet school districts are still claiming they're underfunded, citing declining enrollment, expired federal COVID relief funds, and inflation.

Washington's student population dropped by nearly 48,000 since 2019-20. Funding is tied to enrollment. When you have fewer students but similar fixed costs, the math gets harder—but that's exactly when per-student spending should be going up, not down.

And it is going up. The state now spends $19,000 per student on average, compared to $10,000 before McCleary.

So why the budget crises? One clue: The percentage of the state general fund dedicated to K-12 education dropped from 52.4% five years ago to about 43.1% today. The state budget grew faster than education's share of it.

The Real Story: Property Taxes as Protected Revenue

This is where McCleary connects to something bigger—the structure of Washington's tax system itself.

Property taxes are the state's largest revenue stream at roughly $18 billion annually. The capital gains tax generates about $200 million. The proposed wealth tax would generate roughly $3 billion.

McCleary locked in property taxes as the primary funding mechanism for education—Washington's largest constitutional obligation. The court didn't order an income tax. It didn't order a wealth tax. It ordered "regular and dependable tax sources."

Translation: property taxes.

Every time a school district goes to voters for a levy, they're reinforcing the property tax as the politically acceptable way to fund public services. Every parent who votes yes on a school levy has just validated the property tax system.

This is why real estate remains exempt from the capital gains tax. This is why real estate would likely be exempt from a millionaire tax. Not because of lobbying—because property taxes are the foundation of the entire system, and education funding is the lock that holds it in place.

What You Need To Know

- Your property taxes went up because of McCleary. The state shift from local to state funding was really a shift in which line of your tax bill says "education"—but the total amount increased.

- The levy caps didn't last. Districts can now ask for more local money on top of the increased state funding. Both went up.

- The spending increase is real. From $10,000 to $19,000 per student in a decade. Whether that translates to better outcomes is a different question.

- The system creates a built-in pressure for more. Enrollment goes down, but costs don't drop proportionally. Every budget cycle becomes a crisis that demands more revenue.

- Property taxes are structurally protected. Education funding is the constitutional mandate that makes property taxes politically untouchable. That's not an accident.

The McCleary decision was supposed to fix education funding inequity. Instead, it restructured Washington's tax system to ensure property taxes remain the dominant revenue source—and set up a funding mechanism that guarantees perpetual pressure for increases.

The constitution says education is the state's "paramount duty." What it doesn't say is how much that duty costs—or whose property tax bill will pay for it.

This investigation is part of a larger series examining Washington State's tax structure and the mechanisms that protect property tax revenue. Future installments will examine the relationship between property tax exemptions, the capital gains tax, and the proposed wealth tax.

Sources & Data

McCleary v. State of Washington, 269 P.3d 227 (Wash. 2012)

Washington Supreme Court case documents: courts.wa.gov

Senate Ways & Means Committee, "Overview of Washington's Tax" (2024)

Washington Education Association, "McCleary School Funding"

The Seattle Times, "Post McCleary, WA school funding doesn't add up" (2023)

The Center Square, "WA school leaders make case for more spending" (2024)

Washington State Office of Financial Management expenditure data

King County Assessor property tax data

Comments